20th April 2021

South West Businesses Piling on Debt, Bills and Overdrafts Mounting During Lockdown

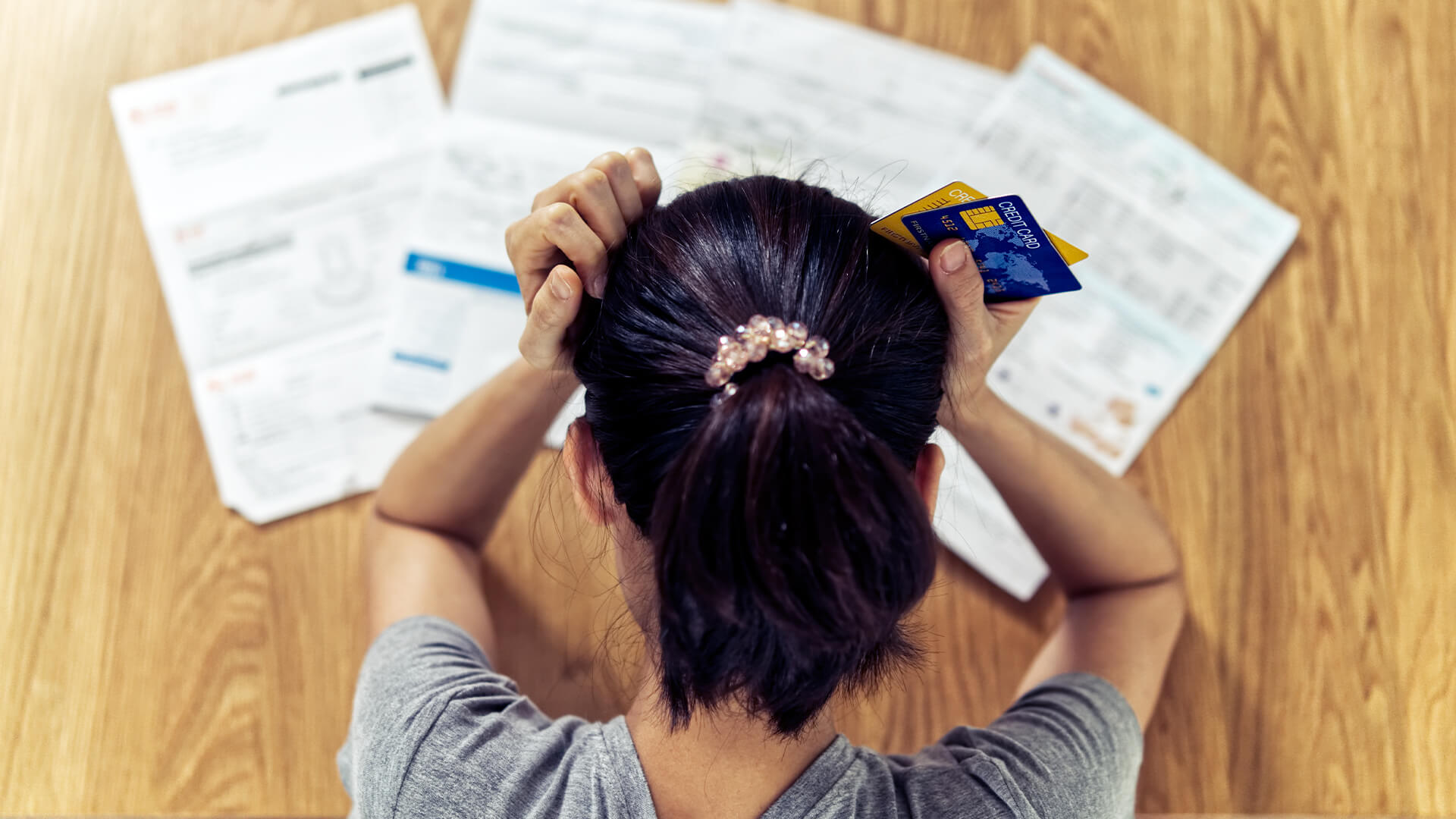

A year on from the start of the pandemic, business finances in the South West have been badly damaged, with many business owners increasingly reliant upon costly sources of borrowing such as overdrafts and credit cards, a Business West survey has revealed.

Scroll

Quarterly Newsletter

Sign up to our quarterly newsletter to receive the latest and most relevant updates, interviews and opinions from finance’s leading lights.

Subscribe

Explore Previous Issues

View the latest issue of the Wealth & Finance digital magazine which features business profiles of leading industry insiders who are thriving in the finance and investment sector.

See Latest Issues

Other Articles You Might Like

Articles16th February 2015Research Reveals Top 10 Questions New SMEs Have

Thousands of people have started new businesses already this year. For anyone thinking of starting a new business, there are some questions you need to know the answer for before you get going.

Articles14th March 2019Bitcoin: Stability Not Likely For Burgeoning Investment Product

Since it first became accepted as an investment product, Bitcoin and other cryptocurrencies have been fluctuating in price and popularity, going from a viable replacement for cash and credit cards through to merely another flash-in-the-pan concept. Hannah Stevenson, Staff Writer, shares an insight into this product and how its value has changed since it first […]

Articles15th January 2015British SMEs Thriving and Growing

British SMEs are thriving with business owners reporting that profits are up in the past year and the outlook is positive.

Articles24th October 2016Understanding the Pound’s Flash Crash: What Triggered It?

For traders, economists, and British citizens, the morning of Friday 7th October 2016 started with a bang. As the Asian session kicked into action, the value of the pound suddenly and mysteriously dropped by an astonishing 10 per cent. This fall occurred in a matter of minutes, leaving spectators open-mouthed with shock.

Articles22nd March 2016UK’s Failing SMEs fall into £1 billion Funding gap, Despite £126 Billion in Untapped Private Investor Finance

Investor confidence in private equity investment is high, with 63% intending to invest in SMEs in the next five years and over half of UK investors looking to EIS for 2016.

Articles27th September 2023Why is Financial Forecasting Important for All Businesses?

Steering a business without a clear vision of the future is like navigating uncharted waters without a compass. Financial forecasting can provide you with direction.

Articles6th January 2014Guernsey adds 33 new funds in Q3 2013

Guernsey’s financial services regulator approved 33 new investment funds during the third quarter of 2013.

Articles3rd February 2021Investing Full Time: What You Need to Know

Investments. A broad term that can be used to describe the purchase of a large form of collateral, such as a house or other class of asset. Or smaller item investments can also be used to describe a luxury watch, a prime example of this is when an Air Force Vet purchased a ‘Cosmograph Daytona Oyster Rolex’ back in 1974 for $350, later to find out the exact model is now worth $700,000 in 2020.

Articles16th January 2015Eurozone’s Trade Balance Improves but Overall Situation Remains Alarmingly Bleak

The Eurozone posted a trade in goods surplus against the rest of the world of €20 billion in November 2014, according to a recent Eurostat estimate.

Articles25th January 2022Confirmation of Payee for Bacs Is a Welcome Upgrade, But It Could Go Further

More than 4.5 billion Bacs payments are made in the UK every year, representing roughly 90% of all regular monthly payments via direct debit transactions. But until now, this vital payment system was not secured by Confirmation of Payee (CoP), a payment verification service that Pay.UK first rolled out in 2020.